|

Tax Considerations

WARNING: We do not have expertise in tax matters and we are not qualified to give tax advise. All viewers of this information, including prospective and existing clients should use it as a starting point for consultations with their professional tax advisor. Please see Disclosures & Backtesting Results Disclaimer. For tax-deferred accounts, like traditional IRAs or SEPs or tax-free accounts, like Roth IRAs, the analysis in this section is not relevant! This only applies to taxable accounts. Why Taxes Are Important Assuming assets generally appreciate, taxes become important in that the amount paid reduces the opportunity to compound returns. As an example, compare two investors. Investor A holds an investment over a long period, say 30 years, and is not required to pay taxes until he sells. Another, Investor B, invests in similar assets and over the 30 year period sells at the end of each year and buys new, similar assets. Investor B will need to pay capital gains taxes, each year, while Investor A won’t. Investor A has the advantage because he is able to compound returns on his tax liability. (However, at the end of the 30 year period, Investor A has a tax liability and when he sells, he will need to pay taxes on his gains). Methodology For Assessing The Impact Of Taxes On Our Strategies Versus Buy & Hold The basic methodology we used was to quantify how much more our strategies would need to return on an after-tax basis to equal the returns of a typical Buy & Hold strategy. While we believe our analysis is useful, taxes paid are highly dependent on your individual circumstances and you should rely on a professional for advice. Key Assumptions: Conceptually, in order to compare our various strategies with a Buy & Hold strategy, needed to make a number of important, simplifying assumptions regarding the tax timing, mix of short-term and long-term gains, and treatment of dividends. These assumptions were slightly different for each strategy: Safeguard 1st Strategy vs. Buy & Hold Strategy Assumptions:

Large Cap Momentum Strategy vs. Buy & Hold Strategy Assumptions:

Small Cap Momentum Strategy vs. Buy & Hold Strategy Assumptions:

High Turn Momentum Strategy vs. Buy & Hold Strategy Assumptions:

Tax Rate Assumptions: Our analysis uses the highest federal tax bracket, full payment of the Obamacare surtax and the assumption that our investors live in high-tax California: in other words, the worst case:

Results Below we provide our results. If you are evaluating the use of our strategies for some of your taxable accounts, you can use the numbers below to make a rough apples-to-apples comparison with Buy & Hold by subtracting the percentage below from the annualized returns of our strategies. For each strategy, we include results under three scenarios: the Buy & Hold investor liquidates at the end of 25, 30 and 35 years. Taxes paid are highly dependent on your individual circumstances and you should rely on a professional for advice. Again, for tax-deferred accounts, like traditional IRAs or SEPs or tax-free accounts, like Roth IRAs, the analysis in this section is not relevant! This only applies to taxable accounts. Additional Before-Tax Annualized Return (CAGR) Required for Our Strategies to Equal a Buy & Hold Strategy: Safeguard 1st Strategy Compared with Buy & Hold

Large Cap Momentum Strategy Compared with Buy & Hold

Small Cap Momentum Strategy Compared with Buy & Hold

High Turn Momentum Strategy Compared with Buy & Hold

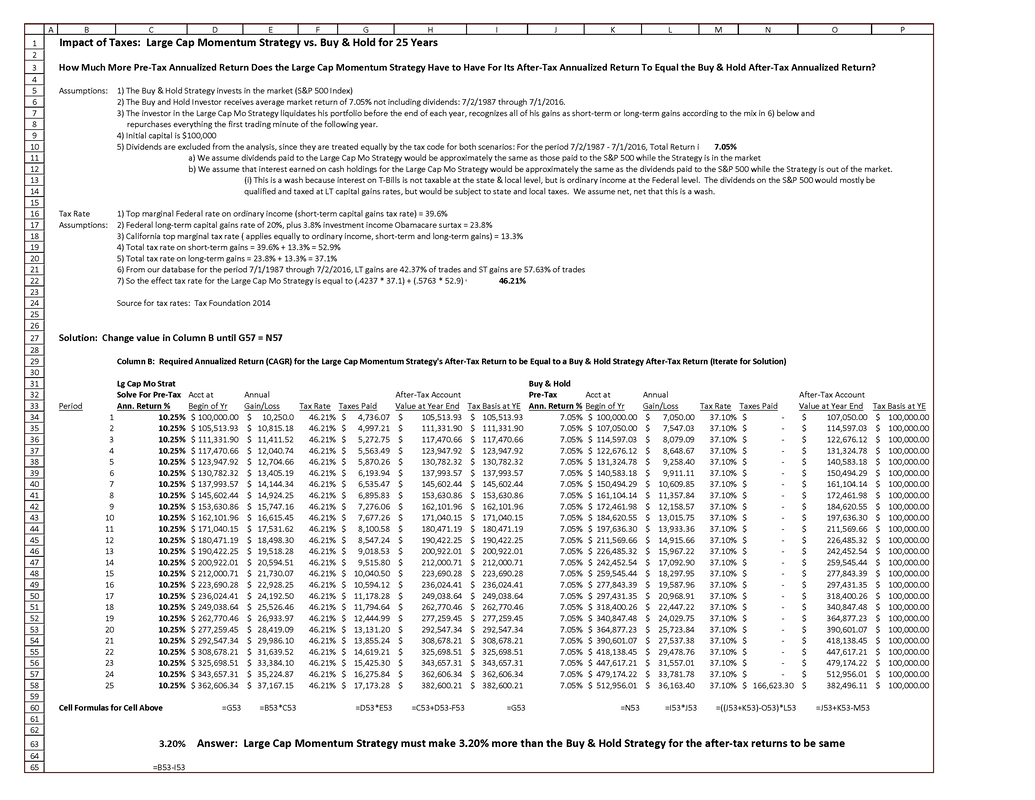

A spreadsheet that demonstrates the calculations described above for the Large Cap Momentum strategy is below. (Click to enlarge). We are happy to share the details of our analysis with prospective clients and/or their tax advisors. |

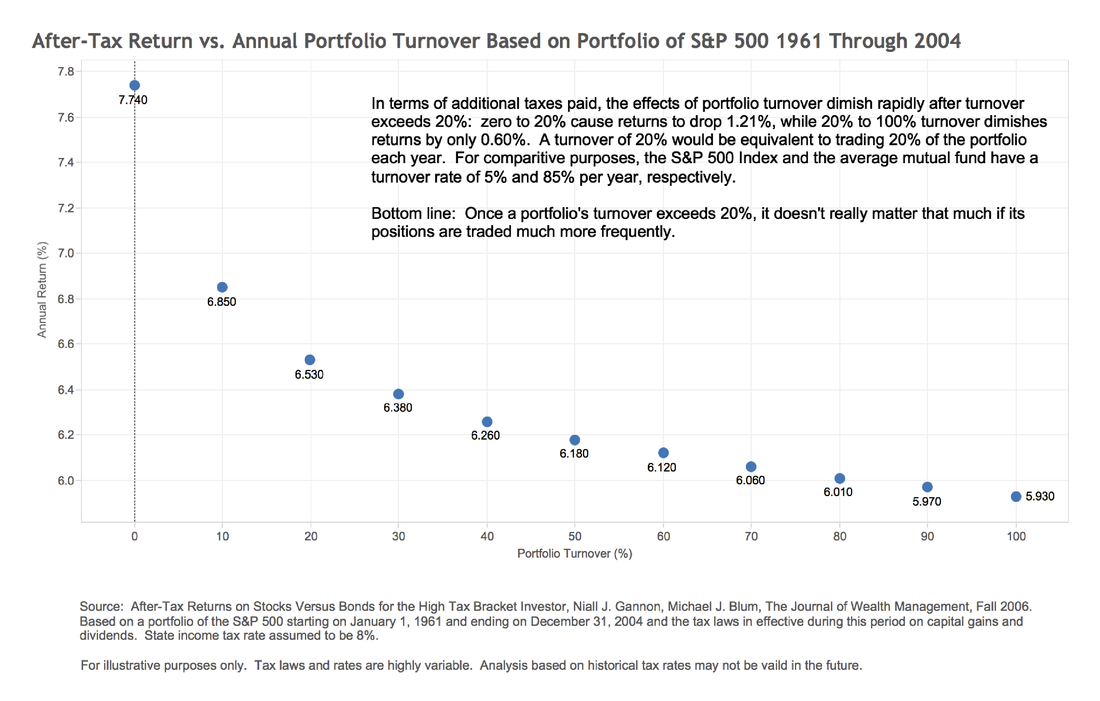

How Turnover of Positions Effects Taxes Paid Many claim that excessive turnover of portfolio investments dramatically reduces returns because of the tax bill that is generated. One interesting finding of our research is that once you deviate from pure Buy & Hold, you lose much of the tax advantages of a Buy & Hold Strategy. Take a look at the chart below. The steepest loss of returns occurs due to the first 5-10% of turnover. Once a portfolio’s turnover exceeds 20% per year, it really doesn’t matter if positions are traded much more frequently. |