|

Fees Matter

Wealth mangers frequently recommend alternative investments to provide diversity in an investment portfolio, but finding a cost efficient way to get this diversity is challenging. Alternative investments generally include assets like private equity, real estate, hedge funds, and commodities. These investments are “alternatives” to stocks and bonds. A portfolio with exposure to alternatives (typically advisors recommend up to 20% or more) may outperform and/or experience less volatility than a conventional portfolio of stocks and bonds. |

|

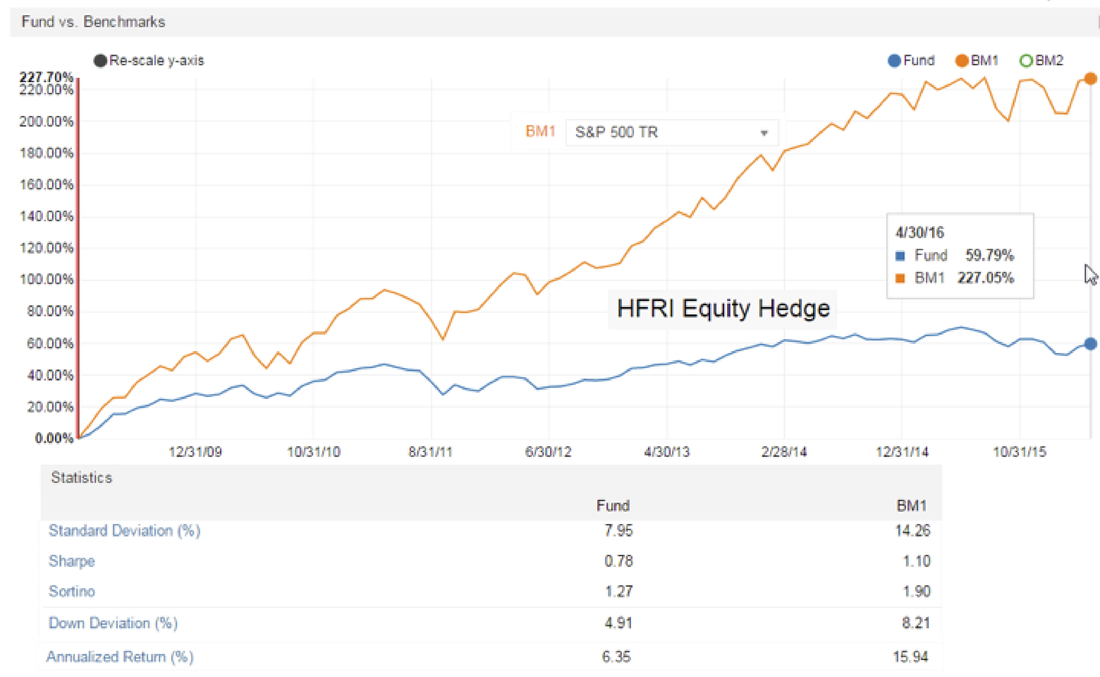

In many ways we consider our strategies to be alternative investments that will reduce risk. Because our strategies go to cash when markets become uncertain, they have low correlations (0.37 to 0.68) to the S&P 500 Index. As such we view our competition as Private Equity, Hedge Funds and REITs, and to a lesser extent stock mutual funds. The advantages we offer to our investors over other alternative investments are

Private Equity and Hedge Fund Fees Alternative investments like private equity and hedge funds have become synonymous with high fees (2% to 5%) and high investment minimums ($500,000 to $5,000,000). Many alternative investments are structured as a fund with management fees of “2 & 20”—meaning 2% in an annual asset management fee and 20% of the profit share. Some studies of this fee structure have concluded that the lofty fees aren’t justified, as the vast majority of these funds do not beat the market or significantly reduce risk. Ironically, this research shows what, in retrospect, is obvious: over the long term, the higher the fees; the lower the net performance. To be fair, it is important to note that some private equity and hedge fund firms have consistently outperformed the stock market after taking fees into account. Hedge funds and private equity funds have targeted the wealthy with promises of high returns and “inside edge” exclusivity via high minimums. The high-touch nature of these investments combined with the opacity of their fee structures have made many revere and assume projected alpha, undeservedly, especially considering the fact that investments/capital commitments are not liquid. Does this performance warrant high fees?

|

|

REIT Fees As for non-traded REITs, according to information on the Investment Program Association website, most non-traded REITs come with front-end fees ranging from 12% to 15% and could feature other fees over the life of the investment. Mutual Fund Fees We don’t know how many of our readers own mutual funds, but if you do, please consider the following on the fees they charge (Please note this does not apply to low-cost index funds, like Vanguard). Costs related to mutual funds are mainly composed of expense ratios, transaction costs, taxes paid by investors and commissions charged by “low fee” advisors. Expense Ratio: The ultimate cost of owning a fund is far greater than what meets the eye. The average mutual fund expense ratio in 2013 was 1.25 percent according to Morningstar, but only about a third of the total cost is reported by the expense ratio. Other hidden fees can more than triple this explicit expense. Including all of the hidden fees associated with mutual funds, the total cost of ownership is estimated to be over 4 percent annually for a taxable account, according to a 2011 Forbes piece, "The Real Cost of Owning a Mutual Fund." It's no wonder so many active managers have lagged their benchmarks and retail investors have flocked to low-cost exchange-traded funds. What makes this even more appalling is the number of surviving stock and bond mutual funds that beat their respective benchmark indices over the ten-year period ending in 2013 was only 19% and 15%, respectively. And this does not account for higher tax liabilities typically generated by actively managed funds, nor the survivorship bias in the numbers, which is huge. Transaction Costs: A 2007 study by Edelen, Evans and Kadlec found U.S. stock mutual funds have an average transaction cost of 1.44 percent per year, which is not included in the expense ratio. These fees are not found in most prospectuses and can be difficult to determine. The first part of these fees is the commission paid to the broker. This alone costs investors roughly 0.25 percent, or 25 basis points each year. It’s important to note most mutual funds don’t pay the rock-bottom, sub-$10 commissions you see advertised from online brokers. Rather, they pay a grossed-up commission, referred to as “soft dollars.” In return for paying this premium, mutual funds get access to research, analysts, management teams and even financial terminals and software. Another factor is the bid-ask spread, which is the difference in price between what the dealer will buy and sell a stock. Even a spread of a penny allows the dealer to capture a fraction of a cent on every share traded. This tiny expense adds another 23 basis points each year. The final piece of the unreported transaction cost is a consequence of the fund’s size. When a portfolio manager decides to trade a position, the large volume is enough to influence the market price. Before the entire order can be sold, the heavy volume drives down the price and a portion of the shares are sold at the lower price, or vice versa for a purchase order. This negative impact costs investors another 96 basis points on average. Taxes: Investors with taxable accounts end up paying more than their share when investing in mutual funds. It is estimated that these cost investors an additional 1 percent per year (for equity funds), according to a 2010 Morningstar article by its fund analyst Katie Rushkewicz. Dollars typically flock to funds with the best performance. In order to build a favorable track record, the manager must have investments that increase in value, and thus have accumulated unrealized gains. When these gains are realized when the investment is sold, owners of the fund must pay capital gains taxes. Unfortunately, this applies to the total gain realized by the fund, even if the investor entered after the stocks appreciated. In total, these hidden expenses create an estimated all-in cost of 4.52 percent for a taxable investor or 3.52 percent for non-taxable accounts. The total cost of mutual fund ownership lowers the annual rate of return from a potential 7 percent to 2.48 percent. “Low-Fee” Advisors: This erosion of wealth does not even incorporate fees paid to a financial advisor. Some advisors pride themselves on having low fees, as low as 25 basis points. These “low-fee” advisors very commonly invest in mutual funds and often receive additional compensation. Symbiosis between the advisor and the fund company is not too dissimilar from soft-dollar arrangements. Assuming a $10,000 initial investment compounded over 30 years if an investor uses a “low-fee” advisor, the ultimate investment would amount to $420,000, benefiting his advisor to the tune of $17,000. It is worth finding an advisor who invests in individual securities, even if the fee is higher. If the same investor chose an advisor who charged 2 percent but did not use mutual funds, after 30 years they would have $664,000 or $244,000 more than using a “low-fee” advisor. Sources: “The Mutual Fund Fees We Don’t Talk About,” Brett Carson, CFA, usnews.com, March 4, 2015 “Mutual Fund Landscape”, Dimensional Fund Advisors, 2014 There are more than 9,000 mutual funds and just 3,700 stocks in the U.S. Do the number of permutations really justify the fees that all of these mutual funds take in? Investment Advisory Fees The largest investment advisors are all broker dealers, which means they charge two types of fees: annual advisory fees and fund fees, which are charged when the purchase funds on your behalf. These estimated fees add up to be as little as 0.38% to as much as 3.5% (see chart below).

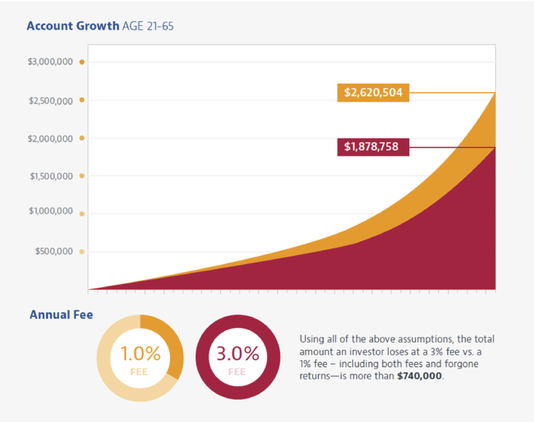

The chart below illustrates the effects that advisor fees can have on a portfolio.

|

|

Key Takeaways Alternative investments, like private equity, hedge funds and REITs often charge high-fees that should be carefully evaluated. If you are in mutual funds with high fees, you may want to consider a Buy & Hold approach with index ETFs, or one of our strategies, which , based on historical data, have provided superior risk-adjusted returns and true diversification at reasonable fees. See Disclosures & Backtesting Disclaimer in the footer of this website. You should always understand the nature and amount of the fees you are being charged for your investments. Fees matter! |