|

Cash Is Not Trash

Introduction Avoiding cash positions in portfolios is a corollary to Buy & Hold investing. The idea is that if you hold cash you may miss out on major portions of bull markets or “you need to put your money to work for you.” As explained elsewhere, going to 100% cash when the market is most risky is a major element of all of our strategies: our first focus is on not losing money. Because our strategies can be 100 percent in cash for considerable periods ranging from a few months to more than two years, we would like to point out the advantages that a cash position brings to a portfolio. Note: Large portions of this section were sourced from www.schwab.com. |

|

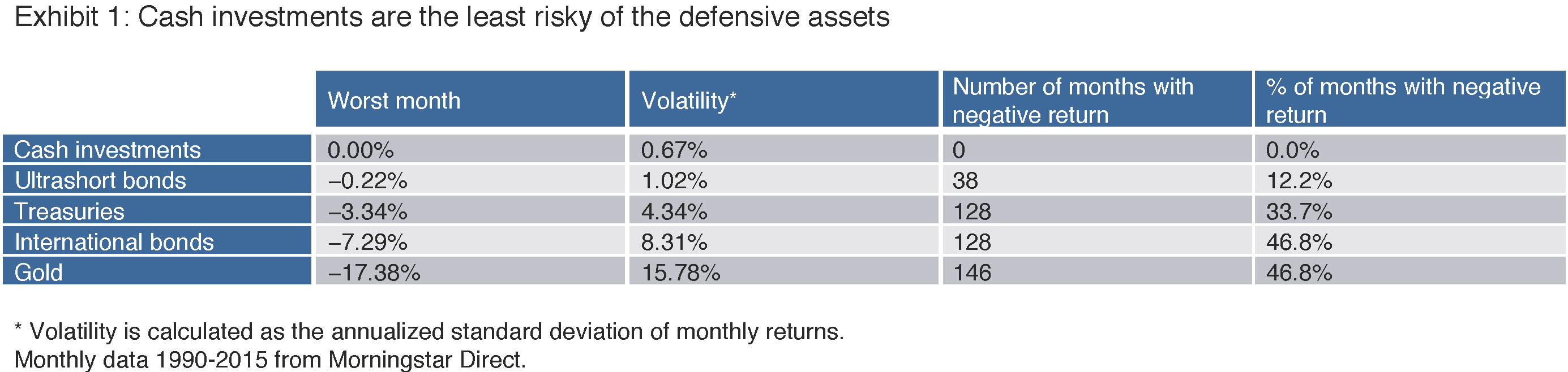

Most investors do not appreciate the power of cash to reduce risk and most investment professionals want to be fully invested so that their clients are “getting their money’s worth.” It can be hard for wealth managers to justify fees to their clients for investing in cash. Cash Defined Here, cash is defined as investments in 3 Month Treasury Bills. When does cash perform well? Two environments where cash tends to do well relative to other asset classes are periods of rising interest rates and times of stock market turbulence. In periods of rising interest rates, cash has done well historically relative to other asset classes because its duration is so short. Duration measures how sensitive a security is to changes in interest rates, or how much its price is expected to fall when interest rates rise and vice versa. Securities with shorter durations are generally less sensitive to changes in interest rates than securities with longer durations. Cash is also a member of the "defensive asset" club, which includes assets such as ultrashort bonds, US Treasury bonds, international bonds and gold. Defensive asset classes tend to perform well during periods of stock market turbulence, and their price movements generally have relatively low or negative correlations with equity securities. What makes cash unique among other defensive assets is that it has the lowest price volatility of the group. By contrast, some other defensive assets (e.g., gold) have a great deal of price volatility associated with them. When does cash perform poorly? Cash may underperform in a very low interest rate environment where the central bank is keeping short-term interest rates low to stimulate economic growth, such as in the aftermath of the financial crisis in the United States. Since cash is very liquid, the rate paid to investors is generally low compared with the yield on other securities. Although cash does not currently provide the level of yield that it has historically, the Federal Reserve began raising short-term interest rates in 2015. As interest rates increase over time, cash investments would be expected to see an increase in yield, as they have historically in rising rate environments. In the future, cash investments could again be a source of potential income in addition to providing safety and stability within a portfolio. Cash helps moderate downside risk One of the first goals of investing is to protect principal and avoid permanent impairment of capital. In other words, avoid losses. Holding cash mitigates downside risk. Research into the behavioral tendencies of investors has shown that investors often have an emotional definition of risk. For example, investors tend to strongly prefer avoiding losses to acquiring gains, a phenomenon known as loss aversion. In fact, studies suggest that the psychological pain investors feel from a loss is twice as strong as the joy they receive from a similar size gain. *Source: Kahneman, D. and Tversky, A. (1984). “Choices, Values, and Frames”. American Psychologist 39, pages 341-350 Cash investments are less volatile (have the least risk) of the possible defensive assets Examples of defensive assets include ultrashort bonds, Treasury securities, gold, international developed bonds, and cash. While each of these investments has defensive characteristics, cash provides the most stability, as illustrated in Exhibit 1.

|

|

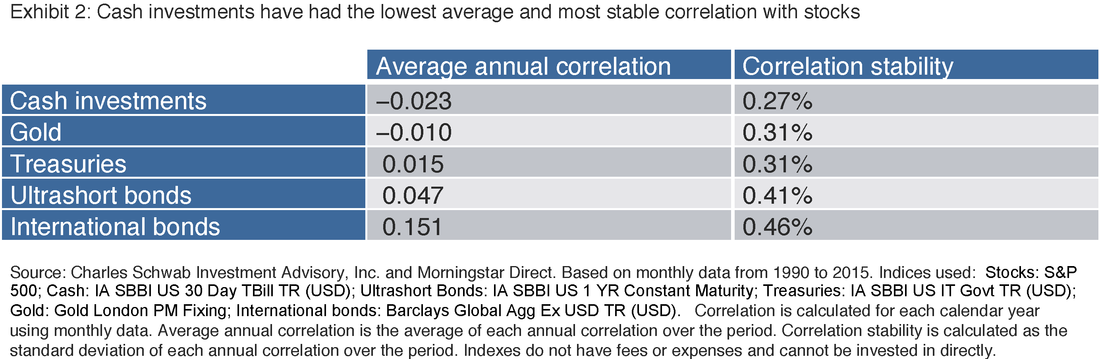

Cash is the best diversifier of stock market risk As illustrated in Exhibit 2, cash investments had the lowest average correlation relative to stocks among the defensive asset classes examined. Additionally, cash investments showed the most stable correlation relative to stocks over the period examined, as measured by standard deviation of annualized correlations. Correlations among asset classes can be highly unstable over time. And in times of market stress, correlations among asset classes tend to rise significantly, providing the least amount of diversification at precisely the time when investors need it most. Given that instability, it is notable that cash delivered the most stable correlation over time, with a standard deviation of the annual correlation of cash investments relative to stocks at 0.27% over the period from 1990 to 2015. We acknowledge that the other defensive asset classes also had relatively low standard deviation of correlations. However, cash investments held the top ranking of both lowest average annual correlation as well as most stable correlation over time, demonstrating that it was the strongest diversifier of stock market risk relative to the other defensive assets.

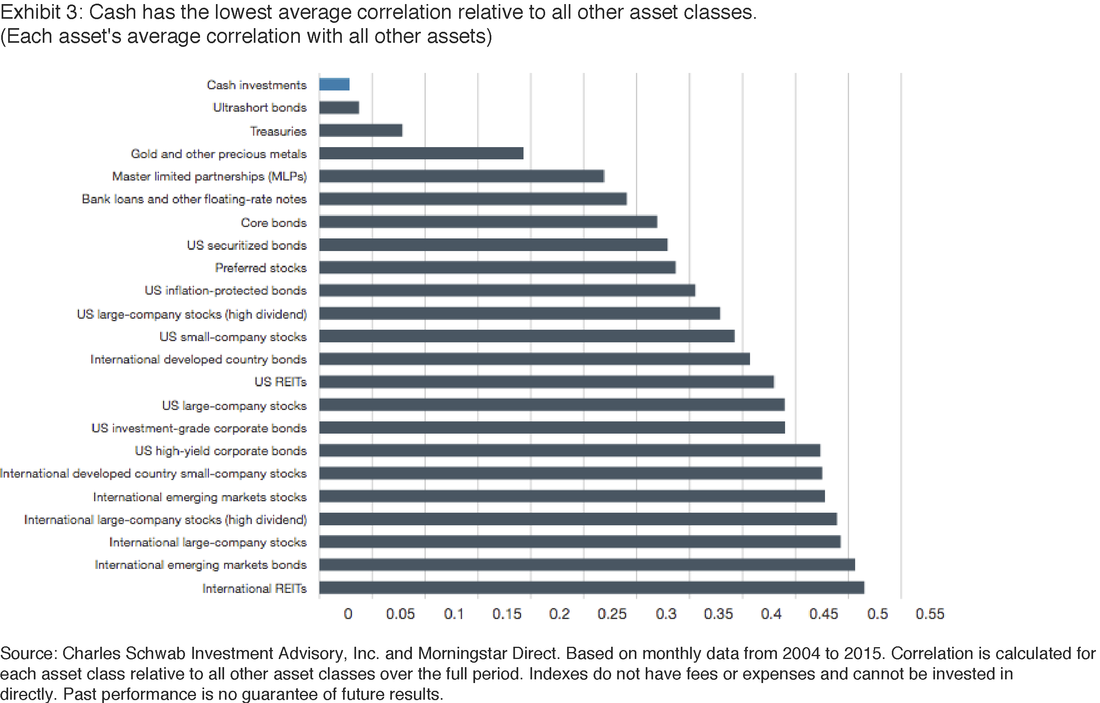

Cash investments are an all-purpose portfolio diversifier as well Also notable is that cash investments represent an all-purpose diversifier relative to other asset classes—not just stocks. Exhibit 3 shows the average correlation for each asset class relative to all of the other asset classes. As the chart illustrates, among all of the assets examined, cash had the lowest average correlation relative to all the other asset classes, reinforcing our argument that it could be wise to have a strategy for a portion of your portfolio that goes to cash when things get risky.

|

|

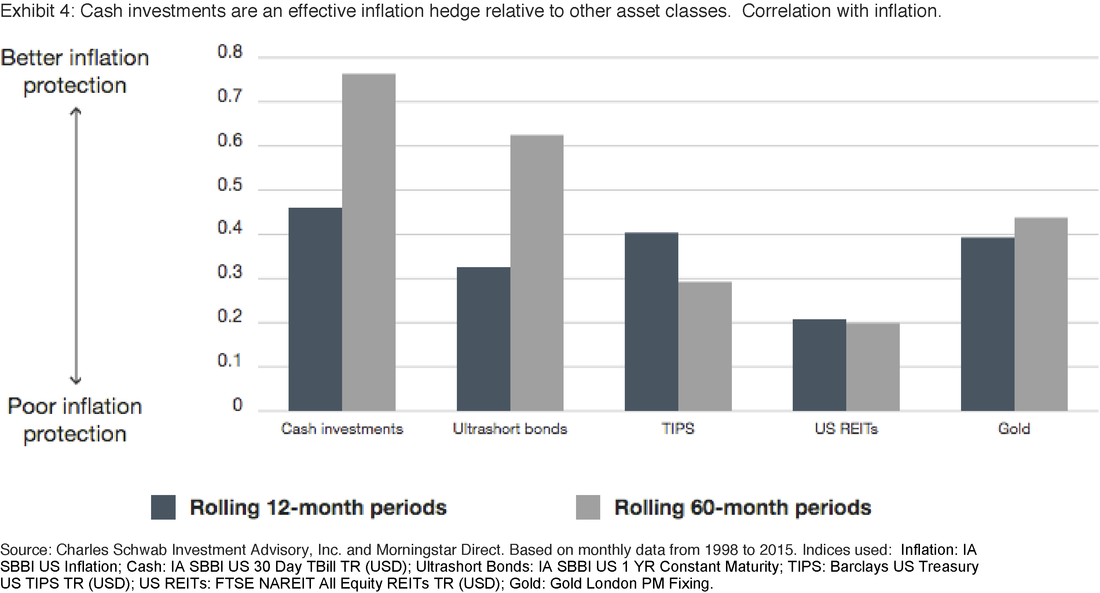

Cash offers better protection against inflation than most defensive asset classes in both the short and long-term Although interest rates and inflation are at generationally low levels today, it is instructive to remember that this environment is a relatively recent phenomenon. With the Federal Reserve beginning to normalize monetary policy and raising short-term interest rates in 2015, interest rates could be headed higher going forward. In an environment of potentially higher interest rates and higher inflation in the future, cash investments may see higher yields and may provide more of the income potential they have historically delivered. Investors have typically turned to several asset classes to help protect a portfolio from potential inflation: inflation-protected bonds (TIPS), real estate and commodities. Although cash investments are not typically looked at as "inflation hedges" because of their relatively low returns, their very short duration means that their yields adjust quickly to changes in inflation. As Exhibit 4 shows, among assets considered to provide inflation protection, cash investments actually have the highest correlation with inflation in both the short and long term. Because cash investments have very short durations, they tend to have minimal negative price sensitivity to rising interest rates, which typically accompanies inflation. Additionally, in a portfolio context, the yield on cash investments tends to track upward along with rising inflation.

|

|

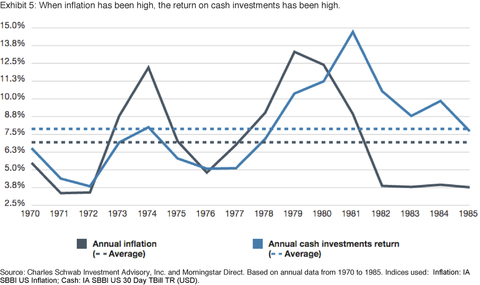

Importantly, cash investments have historically delivered higher returns when inflation was high. As Exhibit 5 illustrates, in historical periods when inflation has been high, the return on cash investments has also been relatively high. Over the period from 1970 to 1985, when inflation rose into double-digit territory, the return on cash rose along with inflation. And over the full 15-year period, the average return on cash of about 8% was higher than the average rate of inflation at approximately 7%. |

Key Takeaways Our strategies are focused first on not losing money and our belief is that one of the safest ways to preserve capital is to go 100% to cash when the market environment is one of high risk. Historically, cash has been the best portfolio diversifier and outperformed when markets became unstable, during bear markets, when interest rates rose, and when inflation was high. Although interest rates and inflation are at generationally low levels today, it is instructive to remember that this environment is a relatively recent phenomenon that hasn’t been seen since the 1950s. With the Federal Reserve beginning to normalize monetary policy, we may experience a number of cyclical bear markets in the future where, because of rising interest rates, bonds and other financial assets severely underperform creating major portfolio losses. Wouldn’t you want a portion of your total investable assets to go to cash when financial markets enter periods of high risk? |