|

Sharpe Ratio

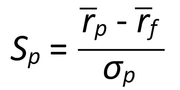

The Sharpe Ratio is a popular measure of risk-adjusting returns for comparing two investments. It measures the return in excess of the risk-free rate divided by the volatility of that investment. It therefore shows the ratio of return “per unit of risk.” Generally, the greater the value of the Sharpe ratio, the more attractive the risk-adjusted return compared to the benchmark. For the more mathematically minded, the equation for the Sharpe Ratio: |

|

|

Where Sp = Sharpe Ratio Rp = The Average Period Return Rf = The Average Risk-Free Rate σp = Standard Deviation of the Portfolio or Asset Returns |